In "6 ways boomer women can get retirement savings on track" Melody Juge gives advice to single, divorced or widowed boomer women. She provides excellent advice at http://www.marketwatch.com/story/6-ways-boomer-women-can-get-retirement-savings-on-track-2014-10-22?page=1. My students discovered you can start an IRA at Schwab for only $100. With the dramatic drop in the price of gas, you can find the money to get started in less than a month.

December 28, 2014

Can you retire on $1 million?

With all the hard core investing and retirement planning info in this blog it's time for a bit of humor, courtesy of John Waggoner of USA Today. "If you read any financial advertising, you know that your savings are

inadequate, and you're likely to freeze to death in the dark a few weeks

after retirement. For this reason, most Americans' retirement planning

involves keeling over at their desks, or, failing that, starting a

bomb-disposal unit as a retirement business." Waggoner goes on to explain some basic concepts essential to understanding the draw-down process of living on your nest egg in retirement and the importance of Social Security. Enjoy learning from his excellent writing: http://www.usatoday.com/story/money/columnist/waggoner/2014/10/23/can-you-retire-with-1-millio/17789939/

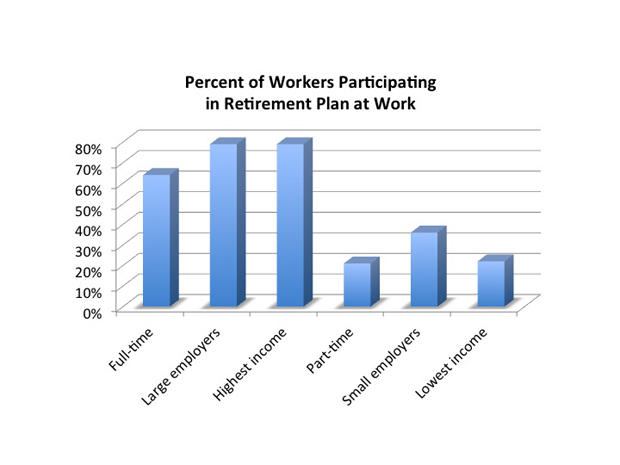

Half of Americans are NOT in a Retirement Plan

According to the US Bureau of Labor Statistics, "just 53 percent of American workers participate in any type of retirement plan at work." Part-time, low-income workers and employees of small businesses are most at risk for not having a plan. Get the details from Steve Vernon: http://www.cbsnews.com/news/half-of-all-american-workers-not-covered-by-a-retirement-plan/

The myRA and Roth IRA plans are options for these workers but many don't earn enough to be able to contribute to a retirement plan. Many of these workers are completely dependent on Social Security when they retire so it is important to strengthen SS NOW and not keep delaying.

The myRA and Roth IRA plans are options for these workers but many don't earn enough to be able to contribute to a retirement plan. Many of these workers are completely dependent on Social Security when they retire so it is important to strengthen SS NOW and not keep delaying.

December 27, 2014

Tax valuation guide for donated goods

The end of the year is a good time to clear out the closets and donate to charity. Homeless shelters are in need of warm clothing, blankets, towels, shoes, boots, and, of course, cash. Kay Bell at Bankrate.com compiled the following guidelines and detailed price lists (on the link below)

"Tax law now requires that all household items given to a charity must be in good or better condition. Those questionable items you donated in previous years and claimed were worth a few dollars because they were in fair condition are no longer acceptable.

Several computer software programs are available to help you figure the tax value of your goodwill. But many people still prefer to use pen and paper, jotting down the item and its worth as they are pulling it from the closet or dresser drawer. If that's your style, the following list will give you an idea of what your donated clothing and household goods are worth. It indicates fair market value for some common items as suggested in the Salvation Army's valuation guide."

"Tax law now requires that all household items given to a charity must be in good or better condition. Those questionable items you donated in previous years and claimed were worth a few dollars because they were in fair condition are no longer acceptable.

Several computer software programs are available to help you figure the tax value of your goodwill. But many people still prefer to use pen and paper, jotting down the item and its worth as they are pulling it from the closet or dresser drawer. If that's your style, the following list will give you an idea of what your donated clothing and household goods are worth. It indicates fair market value for some common items as suggested in the Salvation Army's valuation guide."

Time to Rebalance Your Portfolio!

In light of the raging 5 year bull market, stock prices are at all time highs with the Dow Jones Industrial Average (the Dow) hitting 18,000 on December 23. Now is a great time to rebalance your portfolio by selling high priced stocks (Sell High!) and buying an asset category that has done poorly (Buy Low!) OR shifting to a more conservative asset allocation if you are nearing retirement or other financial goal. As a result of the global financial crisis of 2007-09, the Dow hit rock bottom (6,547) on March 9, 2009 (losing 53% from fall 2007 to March 2009) but has gained 175% since then. According to The Wall Street Journal, the broader S&P 500 tripled in that time span. The past 5 years have been one of the best ever for the stock market. I'm not making a forecast nor am I advocating market timing but I am suggesting that if your asset allocation is a bit too heavy on stocks, now is the time to act to lock in some gains. There is no pattern to stock returns but history suggests that when stocks are over-valued, they are unlikely to continue the current 5 year bull market. According to Spencer Jakab (WSJ 12/26/14, "A white-knuckle ride for stocks") the Shiller P/E is just over 27 which means stocks are very high priced compared to historical measures. "Yale professor Robert Shiller's cyclically-adjusted price/earnings ratio, which takes 10 years of earnings adjusted for inflation, is the best known" and widely respected measure of relative stock prices. Check out the graph for a visual indication that stocks are over-valued: http://www.multpl.com/shiller-pe/. the average Shiller CAPE is 16.58; the median is 15.95. The current value of 27.43 is way up there! Time to lock in some of those gains.

Need more convincing? Read: When the stock market is near record highs, it's more important than ever to think about risk.

http://time.com/money/3537299/investment-advice-you-need-now-risk-stocks-record-high/

Joe Udo provides additional perspective: When to dial down your stock market exposure. http://money.usnews.com/money/blogs/on-retirement/2014/10/23/when-to-dial-down-your-stock-market-exposure

Need more convincing? Read: When the stock market is near record highs, it's more important than ever to think about risk.

http://time.com/money/3537299/investment-advice-you-need-now-risk-stocks-record-high/

Joe Udo provides additional perspective: When to dial down your stock market exposure. http://money.usnews.com/money/blogs/on-retirement/2014/10/23/when-to-dial-down-your-stock-market-exposure

Turn Cheap gas into Retirement Savings

Instead of spending the "savings" from the cheapest gas prices in years, put that money into your retirement account. Spending less at the pump means you have mo ney to invest for retirement. According to the Wall Street Journal, "The typical consumer buys about 600 gallons of gasoline a

year, said

Christopher R. Knittel,

a professor of energy economics at the Massachusetts Institute of

Technology. If gas prices fall a dollar, and remain low, consumers will

pocket $600 over a year, or about $50 each month." If you haven't started an Individual Retirement Account (IRA) yet, now is the perfect time. Or boost your salary deferral in your 401(k) plan at work. You can open an IRA at Schwab for only $100 so stop procrastinating! Fidelity Investments developed the chart below showing how much a budget

windfall could build over time if it were saved for retirement.Thanks to Steve Vernon of MoneyWatch: http://www.cbsnews.com/news/spending-less-on-gas-theres-a-good-use-for-your-savings/

Beware Auto Title Loans

Rise in Loans Linked to Cars Is Hurting Poor, Christmas Day, The New York Times, describes the shift from paydayloans to auto title loans as a way to exploit consumers desperate for cash to pay bills. See: http://dealbook.nytimes.com/2014/12/25/dipping-into-auto-equity-devastates-many-borrowers/?emc=eta1&_r=0

December 24, 2014

Increase your Happiness by Giving

Feel Better by Giving.

Research shows that happiness increases when we spend money on others rather

than ourselves. A great way to give this holiday season is by helping mothers

stay in school and finish their college degree with the USU Center for Women

& Gender's Helping Hands fund: http://womenandgender.usu.edu/helping-hands.html

It's never too late to donate!

Can Money Buy Happiness?

Research shows that people in rich countries like the US are happier than people in poor countries who are struggling to survive. No surprise. In the U.S. and other wealthy countries happiness increases with income up to about $75,000 and then levels off. Basically, once we are financially secure more money doesn't result in more happiness. What really matters is not how much you earn but how you spend.

"life experiences give us more lasting pleasure than material things" Research by Dr. Ryan Howell reveals: “People think that experiences are only going to provide temporary happiness, but they actually provide both more happiness and more lasting value.” "And yet we still keep on buying material things, he says, because they’re tangible and we think we can keep on using them," according to Wall Street Journal writer Andrew Balckman. Cornell University research psychologist Thomas Gilovich has concluded: "Experiences... tend to meet more of our underlying psychological needs. They’re often shared with other people, giving us a greater sense of connection, and they form a bigger part of our sense of identity." “Hedonic adaptation” makes it so hard to buy happiness with possessions. "The new dress or the fancy car provides a brief thrill, but we soon come to take it for granted." we tend to compare our possession but not our experiences with other people. “Keeping up with the Joneses is much more prominent for material things than for experiential things,” Gilovich says. “Imagine you’ve just bought a new computer that you really like, and I show up and say I’ve paid the same amount for one with a brighter monitor and faster processor. How much would that bug you?” Conclusion: spend time with family and friends; avoid the (online or bricks & mortar) mall and reduce your impact on the landfill. Happy Holidays!

"life experiences give us more lasting pleasure than material things" Research by Dr. Ryan Howell reveals: “People think that experiences are only going to provide temporary happiness, but they actually provide both more happiness and more lasting value.” "And yet we still keep on buying material things, he says, because they’re tangible and we think we can keep on using them," according to Wall Street Journal writer Andrew Balckman. Cornell University research psychologist Thomas Gilovich has concluded: "Experiences... tend to meet more of our underlying psychological needs. They’re often shared with other people, giving us a greater sense of connection, and they form a bigger part of our sense of identity." “Hedonic adaptation” makes it so hard to buy happiness with possessions. "The new dress or the fancy car provides a brief thrill, but we soon come to take it for granted." we tend to compare our possession but not our experiences with other people. “Keeping up with the Joneses is much more prominent for material things than for experiential things,” Gilovich says. “Imagine you’ve just bought a new computer that you really like, and I show up and say I’ve paid the same amount for one with a brighter monitor and faster processor. How much would that bug you?” Conclusion: spend time with family and friends; avoid the (online or bricks & mortar) mall and reduce your impact on the landfill. Happy Holidays!

December 23, 2014

What 2,000 calories looks like!

Tthe season of culinary excess calories it's a good time to be reminded to bring a couple of plastic containers to take home some excess calories for tomorrow. It's way to easy to consume an entire days' calories in one meal when eating out. So eat at home more often to save calories and money! Courtesy of The New York Times and

http://www.nytimes.com/interactive/2014/12/22/upshot/what-2000-calories-looks-like.html?emc=eta1&_r=0&abt=0002&abg=1

http://www.nytimes.com/interactive/2014/12/22/upshot/what-2000-calories-looks-like.html?emc=eta1&_r=0&abt=0002&abg=1

Best Squared Away Blog Posts of 2014

It’s a holiday tradition for the Squared Away Blog to feature readers’ favorite articles published during the year. Check them out at: http://squaredawayblog.bc.edu/squared-away/what-readers-liked-in-2014/ and sign up for a weekly email post. Hint: the most popular topic was retirement.

5 ways your retirement money makes money

1. Interest earned

2. Dividend payments

3. Tax deferral

4. Rebalancing

5. Compounding

Mitch Tuchman explains why "time is money" and why you need to start early. It's never too late; today is the first day of the rest of your life so get going! Details at: http://www.forbes.com/sites/mitchelltuchman/2014/12/22/retirement-5-ways-money-makes-money/

2. Dividend payments

3. Tax deferral

4. Rebalancing

5. Compounding

Mitch Tuchman explains why "time is money" and why you need to start early. It's never too late; today is the first day of the rest of your life so get going! Details at: http://www.forbes.com/sites/mitchelltuchman/2014/12/22/retirement-5-ways-money-makes-money/

Evaluate your retirement account in 15 minutes

Do you know how hard your money worked for you in 2014? If not, it's

time to do a 15-minute checkup of your investments and make some plans

for 2015.

Step 1: Check your performance

Step 2: Review the fees

Step 3: Rebalance your assets

Get the details from Maryalene LaPonsie/MoneyTalksNews at: http://www.cbsnews.com/news/how-to-evaluate-your-retirement-accounts-in-15-minutes-or-less/

Step 1: Check your performance

Step 2: Review the fees

Step 3: Rebalance your assets

Get the details from Maryalene LaPonsie/MoneyTalksNews at: http://www.cbsnews.com/news/how-to-evaluate-your-retirement-accounts-in-15-minutes-or-less/

December 19, 2014

The Most Important Question To Ask Your Financial Advisor

"Whether you already have a financial advisor or are now looking to hire

one, you want someone who has your best financial interest at heart.

That means that when she is helping you direct your money and advising

you on financial goals, she’s not just selling you products that she

will be making money on, while you shell out more than need be." This article by Laura Shin may help you understand the complexities of how

the financial industry works:

It is the most thorough and understandable explanation I’ve

read and should be read by everyone who buys investment or advice from a financial salesperson/adviser/planner.

New US Treasury bond for myRA Retirement Accounts

For conservative retirement savers/investors, a new savings bond is available only to participants in

the myRA retirement savings program. "The bonds are designed to protect the

principal contributed while earning interest at a rate previously available

only to federal employees invested in the Government Securities Investment Fund

(G Fund) of the Thrift Savings Plan." Details at: http://www.planadviser.com/NewsArticle.aspx?id=10737424942&p=1

December 18, 2014

Start saving for retirement with myRA

myRA is

a retirement savings account for individuals looking for a simple, safe and affordable

way to save for their retirement. There will be no fees to open and maintain a

myRA and the account will never lose value. The investment will be backed by

the United States Treasury. First you need to convince your employer to participate since myRA accounts can only be funded with direct deposit through an employer.

For additional information visit Treasury’s website: www.myra.treasury.gov and questions can be directed to their email account: myRA@treasury.gov. Federal employees that are eligible to participate in the Thrift Savings Plan are not eligible to participate in MyRA.

For additional information visit Treasury’s website: www.myra.treasury.gov and questions can be directed to their email account: myRA@treasury.gov. Federal employees that are eligible to participate in the Thrift Savings Plan are not eligible to participate in MyRA.

You will be able to learn

valuable information about myRA .

1) Why was myRA developed?

2) Who is myRA for?

3) How does myRA work?

4) How do employers participate?

5) How do individuals get started? And more….

Subscribe to:

Posts (Atom)